“By the age of 30, your net worth should be a minimum of AED1,000,000.” Statements like this now abound, and there is no end to influencers telling people how much they should have made by a certain age.

The problem can be exacerbated if you have friends who have reached that mark already. You begin to feel that you are behind while others are setting their financial lives in order. This can lead to financial stress and anxiety.

For some, worrying about whether you have hit a target net worth is even a luxury. The sources of financial concerns for these people are:

- Living paycheck to paycheck due to the rising cost of living (responsible for 45% of stress in the UAE in 2024)

- Racking up debt just to meet up with monthly living expenses

- Not having enough money to deal with financial emergencies

- Fears of a generational poverty cycle

Unfortunately, financial stress can hamper your mental health, leading to high levels of psychological distress, anxiety disorders, depression, and other health problems. If you desire to live an optimal life, you need to learn how to manage financial stress.

In this article, we will consider how to deal with all kinds of financial stress and set up your finances for financial well-being. We’ll cover:

- Having the right expectations: Separating fact from fiction

- Learning from the past: Avoiding painful mistakes

- Taking control of the present: Setting the right foundation for the future

- Preparing for the future: Taking advantage of the financial market

Do you want to avoid future financial stress by creating wealth through investing? Sign up now for Sarwa’s Fully Invested newsletter for expert investment insights.

1. Having the right expectations: Separating fact from fiction

The best way to deal with stress of any type is to identify the cause(s). It is easier to find a solution when there is clarity about the nature of the problem.

For example, suppose the source of your financial stress is a YouTuber’s perception that you should have a certain net worth by a certain age.

In this case, the first question to ask is how common, on average, it is for people of that age to have that net worth. This is because you will be prone to financial stress if you have unrealistic expectations due to your focus on outliers.

Statistics on the average net worth of UAE residents by age group are scarce.

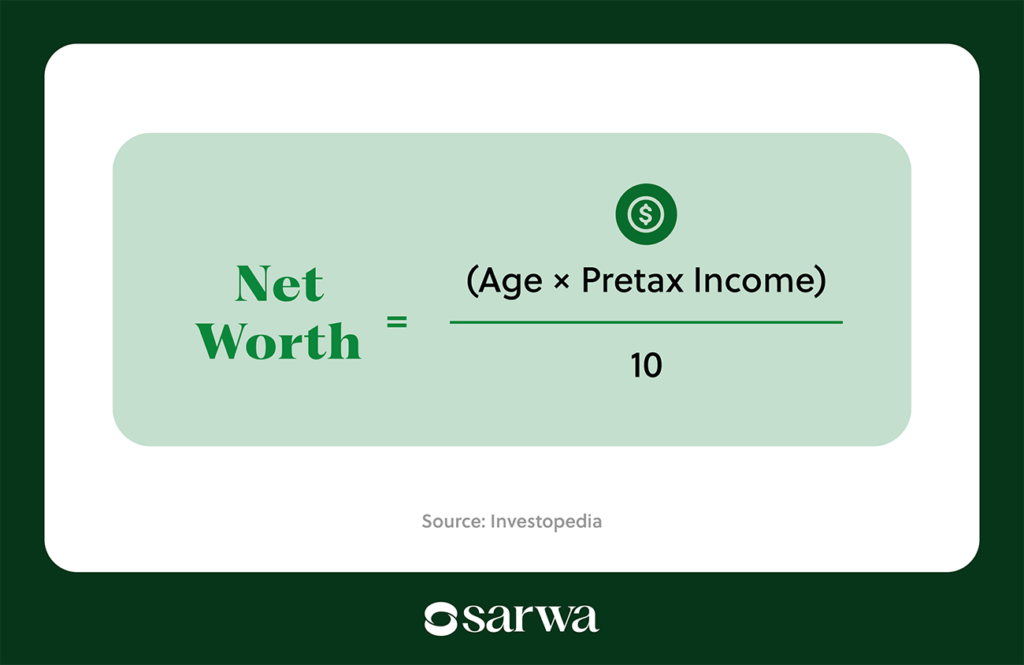

However, many financial advisors follow the rule of thumb provided by Thomas J. Stanley and William D. Danko, authors of “The Millionaire Next Door: The Surprising Secrets of America’s Wealthy.”

According to them, your ideal net worth is calculated by multiplying your age by your annual income, then dividing the result by 10.

Source: Investopedia

Suppose your annual income is AED 180,000 and you are 35, then your ideal net worth is AED 630,000. Does it matter that there is a 35-year-old influencer or celebrity with a net worth of AED 6.3 million? No!

Based on this, if you have a net worth equal to or greater than AED 630,000, you are doing well. You can take a deep breath and stop worrying about what other people are doing.

“Comparison is the thief of joy,” according to a quote attributed to Theodore Roosevelt. Once you have your number, you should focus on it instead of comparing yourself to others.

Similarly, some of the expectations you see on YouTube don’t reflect the general conditions of things but a limited perspective based on the experience of a few people.

Someone might have inherited great wealth, got a very good job at a young age, or bought bitcoin when it was $100. Again, these are outliers, and it’s best to focus on the mean or median distribution when dealing with net worth or wealth expectations.

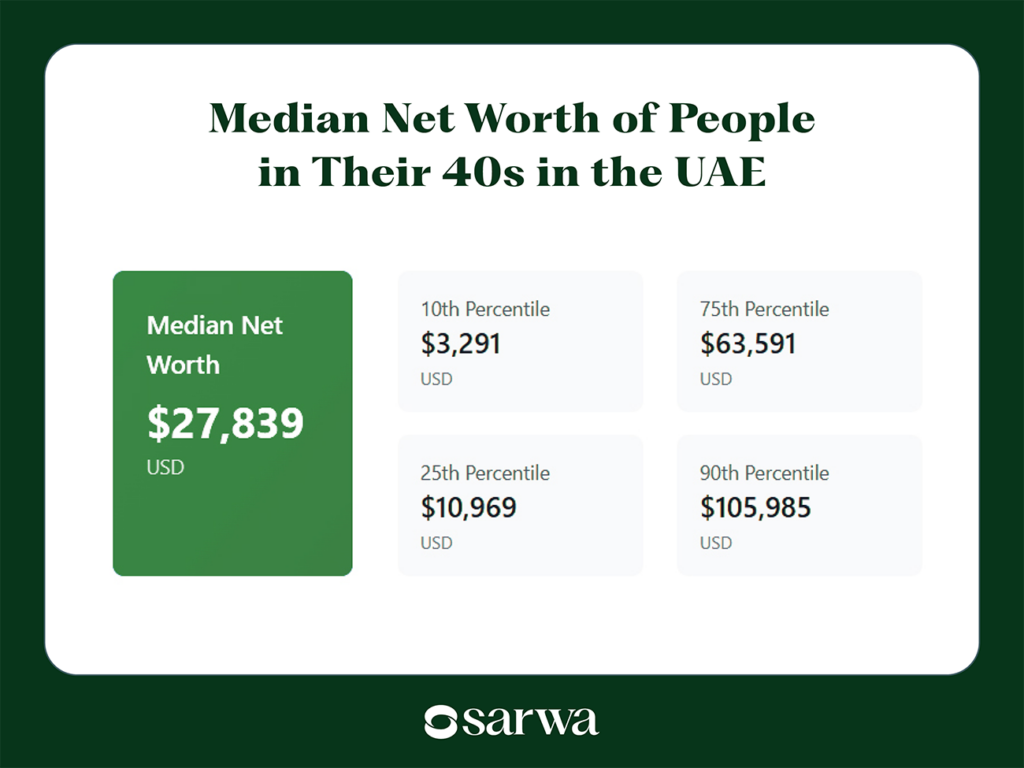

For example, the median net worth of people in their 40s in the UAE is $27,839 (AED102,238.73), according to Bear Savings, a financial planning and savings platform.

Of course, there are people in the top 10% (90th percentile) with a net worth of $105,985 (AED 389,229.91), but these are outliers. And remember that there are also people in the bottom 10% (10th percentile) with a net worth of only $3,291 (AED 12,086.20).

Since we don’t have much standardized data about wealth distribution by age group, your best option is to use the formula by Stanley and Danko, while having realistic expectations about what your age mates are doing.

Doing this will help eliminate one of the key sources of financial stress: the thought that you are falling behind.

2. Learning from the past: Avoiding painful mistakes

Nevertheless, you may be falling short of your ideal net worth when you use the formula above.

However, instead of sliding into stress and anxiety, you should identify the key stressors that have brought you into this situation.

The same goes for the other sources of anxiety we have identified. The first task for those learning how to manage financial stress is to be transparent about the wrong steps they have taken to be in the current situation.

Why are you living from paycheck to paycheck? Is it because you are locked in a low-paying job because you didn’t take that certification exam a few years ago?

Is the reason you are struggling with debt due to your past (and current) attempts to live the same exotic lifestyle your richer friends are living? Or are you struggling with black taxes because you project a false view of your financial situation to your family members?

In essence, what have you done in the past that has complicated your current financial situation? Though these are difficult times, you still need to have these difficult conversations with yourself to gain clarity.

There are 10 common culprits, according to Time Magazine:

- Living beyond your means

- Failing to save for retirement

- Not having an emergency fund

- Overlooking the power of compound interest

- Ignoring high-interest debt

- Not understanding taxes (largely irrelevant in the UAE context)

- Making emotional financial decisions

- Neglecting insurance needs

- Failing to plan for large purchases

- Skipping estate planning

However, the purpose of this evaluation is not to hate yourself for your financial mistakes. The past is gone; we can only learn from its mistakes in search of a better present and future.

So, instead of regretting where you are, take charge of your future by taking the right actions.

(Side note: It is true that some people are so overwhelmed with financial stress that they can’t even take this clarity-seeking step. In such cases, financial stress might have caused mental health issues. Such people might benefit from the services of a mental health professional. Only when they are in a better mental situation can they take money advice and prepare for a better financial future.)

3. Taking control of the present: Setting the right foundation for the future

Now that you know your target and the wrong steps you have taken that have caused money problems, the next step is to forget the past and become better at managing money.

The way to do this is to set the right personal finance foundations for a prosperous future. Going from financial challenges to clarity can be a torturous road, but it is a road that leads to financial peace and overall wellness down the line.

What does this road look like? There are four stopovers on it:

Creating a monthly budget

Nothing is more foundational to personal finance wellness than budgeting.

If you are living paycheck to paycheck, not saving because of emergencies, struggling with debt payment, the solution most times goes back to creating a monthly budget.

This is because a budget will help you spend less than what you earn and create the excess you need to correct your past mistakes and then take steps toward financial freedom.

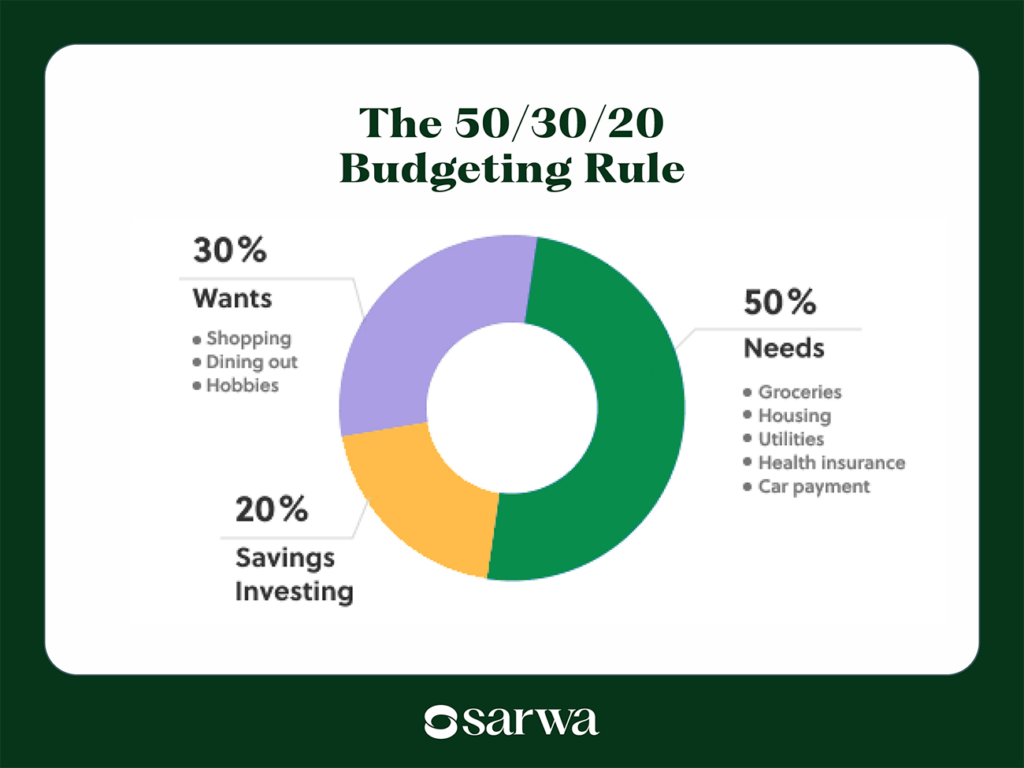

A popular budgeting system is the 50/30/20 rule:

With this system, 50% of your income goes to your needs, 30% to your wants, while the remaining 20% will be for savings/investments.

Your first task is to take a long, hard look at your past spending habits and categorize them into needs and wants. If you are in a difficult place financially, it usually means your needs and wants add up to more than 80% of your income.

If this is so, then you need to start cutting things off, beginning with your wants. This will be a difficult process, but it’s a small price to pay for financial wellness and wealth.

“Look everywhere you can to cut a little bit from your expenses. It will all add up to a meaningful sum,” according to Suze Orman, a financial advisor.

Some of the tips that can help you cut down on your living expenses (needs plus wants) and save money in Dubai include:

- Buy your groceries in bulk

- Reduce restaurant budgets

- Increase your room temperature by 1 degree

- Using a do-it-yourself (DIY) workout program instead of paying for a gym membership

- Time your big purchases around GITEX and the Dubai Shopping Festival

- Renegotiate your rent or move to a more cost-effective place (provided your transport costs won’t escalate)

- Renegotiate the interest rate on your mortgage

- Consider using public transport at times

- Shop around for better value for money

- Save big on TV packages and app subscriptions

- Stop carrying unnecessary cash

Some of these may apply to you, while others may be irrelevant. The point is that you should thoroughly consider ways you can cut down on your living expenses until your needs and wants are at most 80% of your income.

Sticking to a budget

Creating a budget is the easy part. Old habits die hard, they say. In other words, you will be tempted to go back to splurging on some unnecessary items that you enjoy, creating fresh financial problems.

How then can you stick to your budget in those circumstances?

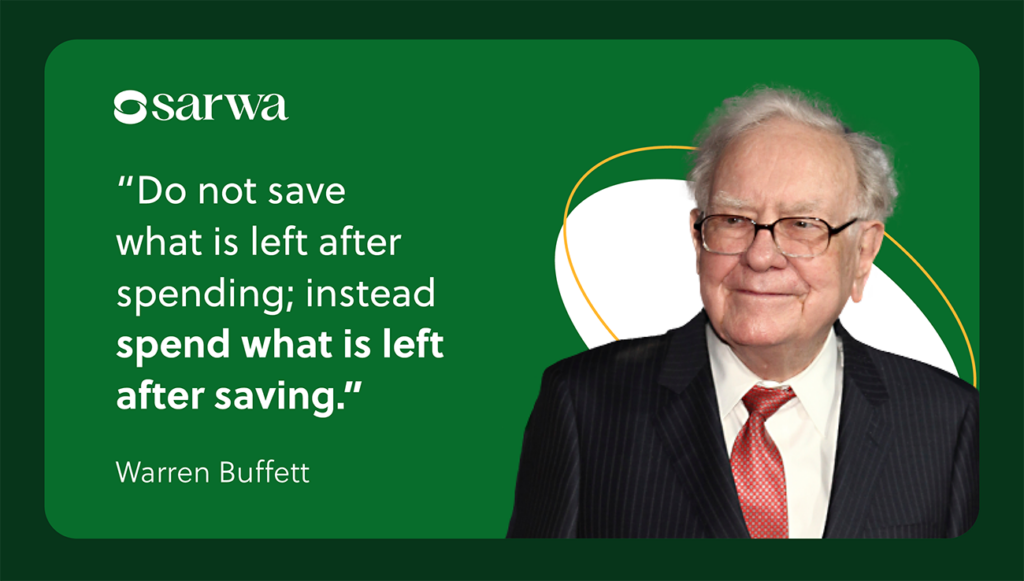

The best thing is for you to save before you spend, as Warren Buffett advised.

If your 20% is going to debt snowballing, creating an emergency fund, saving for short-term goals, or investing in a diversified portfolio, you should send it there before focusing on how to spend the remaining 80%.

Also, at the psychological level, you need to constantly remind yourself that though the path to financial freedom is tough, its joy is better than the emotional drain of financial stress and anxiety.

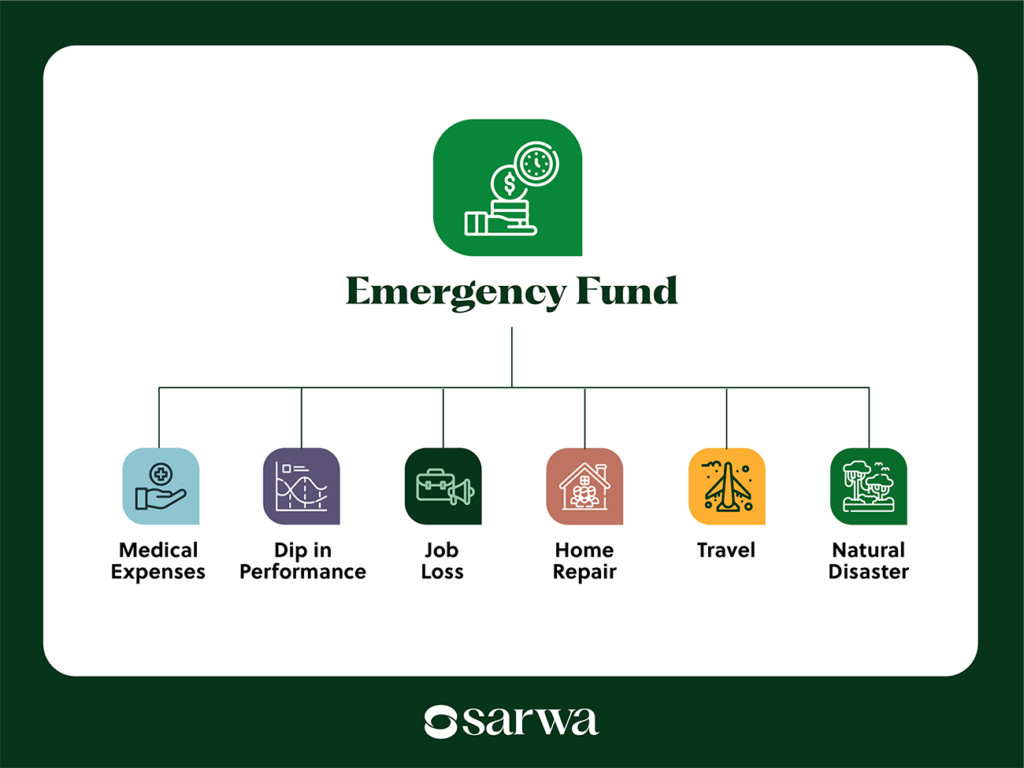

Creating an emergency fund

Financial emergencies are often the primary cause of money worries. These are unexpected expenses and they include unexpected medical expenses (out-of-pocket expenses even when there is insurance), job loss, unplanned travel, dip in business performance, natural disasters, and unexpected car repairs.

Black taxes from dependents are usually another source of financial emergencies.

Many people go into debt because of these emergencies.

The best way to avoid the financial stress that comes from emergencies is to start an emergency fund.

Many financial advisors suggest that you have up to 6-12 months’ worth of your living expenses in such a fund. For example, if your needs and wants add up to AED 10,000 per month, you should have AED 60,000 – 120,000 in an emergency fund.

An emergency fund is revolving, so you will have to replace any amount you spend down the line.

Dealing with high-interest debt

If you have some high-interest debts to pay, then paying them off should be a priority. These are usually credit card debts and other consumer debt.

In fact, since the interest rates on these debts exceed what the stock market will give you (on average), you are better off clearing them before investing.

Also, you should start paying them off before creating a full emergency fund. That is, you can start with a 3-6 months’ emergency fund, pay off these high-interest debts, and then continue with the emergency fund.

The Debt Snowball method, popularized by Dave Ramsey, a US-based financial advisor, is a good place to start from.

The idea is that you should attack the smallest debt first so you can gain the confidence to focus on the bigger ones. If you focus on the biggest debt, you may feel overwhelmed by the entire process.

Some people have even saved more than 20% of their monthly income so they can clear off these debts sooner. Do so if you can.

Once you have paid off these debts, you can then complete your emergency fund. With that, you can be sure emergencies won’t push you into consumer debt again.

Of course, you will still need to develop the discipline to avoid entering into debt to buy the latest iPhone or whatever your weakness is. Always remind yourself of the price you had to pay to clear your debts; it will motivate you to avoid fresh ones.

To clarify, we are talking here about bad debt instead of good debt.

The former include credit card debt, personal loans for non-essential spending, and loans for luxury cars, while the latter include money you spend on things that will increase your future income and net worth (student loans, mortgages, and, to some extent, business loans).

Knowing how to manage financial stress begins with the implementation of these four foundational personal finance strategies.

Once you have the right foundation, you can then move from merely managing financial stress to building wealth and foreclosing future financial stress and anxiety.

4. Preparing for the future: Taking advantage of the financial market

We have focused on how to manage financial stress by learning from the past and setting a good foundation in the present. Now is the time to create a future of financial freedom and independence, which is the ultimate antidote to financial stress.

There are three things you should do in this respect:

Invest in yourself

Though we have focused on trimming down your expenses as the path to setting the right personal finance foundations, there is only so much you can cut.

The primary reason for this focus is that your expenses are under your control and you can cut them immediately.

But there comes a point where you recognize that increasing your income is more important in the long run.

Also, there is a correlation between financial stress and income such that people with lower incomes are more likely to experience stress, according to the American Psychological Association (APA).

Therefore, a part of the 20% you are saving or investing should go into investing in your career so you can command a higher income. This can be in the form of taking some important courses or certifications that can help you climb the corporate ladder.

Explore additional income sources

In addition to investing in your current career, you should explore side hustles and passive income ideas that can help augment your income.

This can include offering your services on freelance platforms like Upwork or Fiverr, becoming an affiliate marketer, dropshipping products, becoming an online tutor, creating content, selling digital products, and becoming an influencer.

Most of these won’t require any significant investments. With just a little investment, you can set yourself up for extra income.

Invest in the financial markets

The higher your income, the more money you have to spend (80% of AED 150,000 is greater than 80% of AED 100,000). But more significantly, the more you have to invest in the financial markets.

A part of the 20% you are saving every month will go to your short-term goals (making the down payment for a property, purchasing a new phone, paying your children’s school fees, buying a new TV, etc.).

You can save money for these short-term goals in a savings account, money market mutual fund, or a high-yield savings product like Sarwa Save.

However, for financial freedom and independence, you need to invest in financial markets like the stock market, where you can build wealth over years and decades.

Let’s take an example to illustrate.

The S&P 500 Index (an index of the 500 largest US companies by market cap) has produced an average annual return of 10.54% between 1957 and 2025. Though past performance does not guarantee future performance, we can confidently use this figure as a benchmark.

Suppose you are consistently investing AED 10,000 every month into an S&P 500 ETF for 10 years. Let’s also assume your investment account compounds quarterly. By the end of the 10th year, your portfolio would be worth AED 2,101,932.89. In other words, you would be a millionaire.

Whether your long-term goal is retiring with a significant nest egg, achieving financial independence, or leaving an estate for your children, investing in the financial markets is the way to do it.

Sarwa Invest Academy – How To Prepare Yourself For Investing

There are two ways to approach this:

First, if you don’t have the time and skills to research assets and build a portfolio on your own, you can invest through managed investment platforms like Sarwa Invest.

These platforms will create a customized portfolio for you based on your financial goals, time horizon, and risk tolerance. Such a portfolio will include assets like stocks, bonds, gold, and real estate investment trusts (REITs), among others.

Second, if you have the time and skills to conduct stock market fundamental and technical analysis, you can learn how to build an investment portfolio from scratch. Here, you will select the assets you want and combine them with your allocation formula.

You can purchase assets like stocks, bonds, REITs, cryptocurrencies, ETFs, gold, and silver, among others, on Sarwa. With such a platform, you can build a portfolio that will help you create the wealth you desire.

Staying put: The psychological aspects

Everything we have said depends on your determination to stick to the plan. Any small detour can cause some financial difficulties that result in a fresh wave of financial worries.

Suppose you emptied your emergency fund to buy the latest iPhone and TV. Two weeks later, an emergency happened. Because you are out of cash, you took a high-interest loan.

Now you can’t invest because the debt servicing has put a strain on your monthly income. Before you can start investing again, you need to rebuild the emergency fund.

Some people hire a financial advisor to help them make financial decisions and keep them from going off-kilter. Others prefer an accountability partner that can provide financial advice and keep them on their toes. Many personal finance apps also have features designed to prevent you from misstepping.

All of these are fine, but you can boycott them all if your resolve is strong enough.

In the end, the best way to stay put is to remind yourself why a life of financial stability, independence, and freedom is better than one of financial strain, anxiety, and stress.

If you are ready to build wealth by investing in the financial markets, Sarwa is a partner you can trust. You can invest passively through our managed investment platform or create your own portfolios on our brokerage platform.

You don’t need to be rich to start investing with Sarwa. With just $500, you can access either of the two platforms and begin your journey to wealth.

Are you ready to secure your financial future? Sign up for a Sarwa account to invest in the financial markets in a cost-effective, seamless, and secure way.

Takeaways

- Unrealistic expectations fuel financial stress. Instead, focus on your own financial path instead of comparing yourself to outliers like influencers or celebrities.

- Clarity reduces anxiety. Identify past financial mistakes, learn from them, and use that insight to build a healthier financial future.

- Financial stability begins with foundations like budgeting, creating an emergency fund, sticking to spending limits, and clearing high-interest debt.

- Long-term financial wellness comes from investing: in yourself, additional income sources, and diversified financial markets through accessible platforms like Sarwa.